In This Article

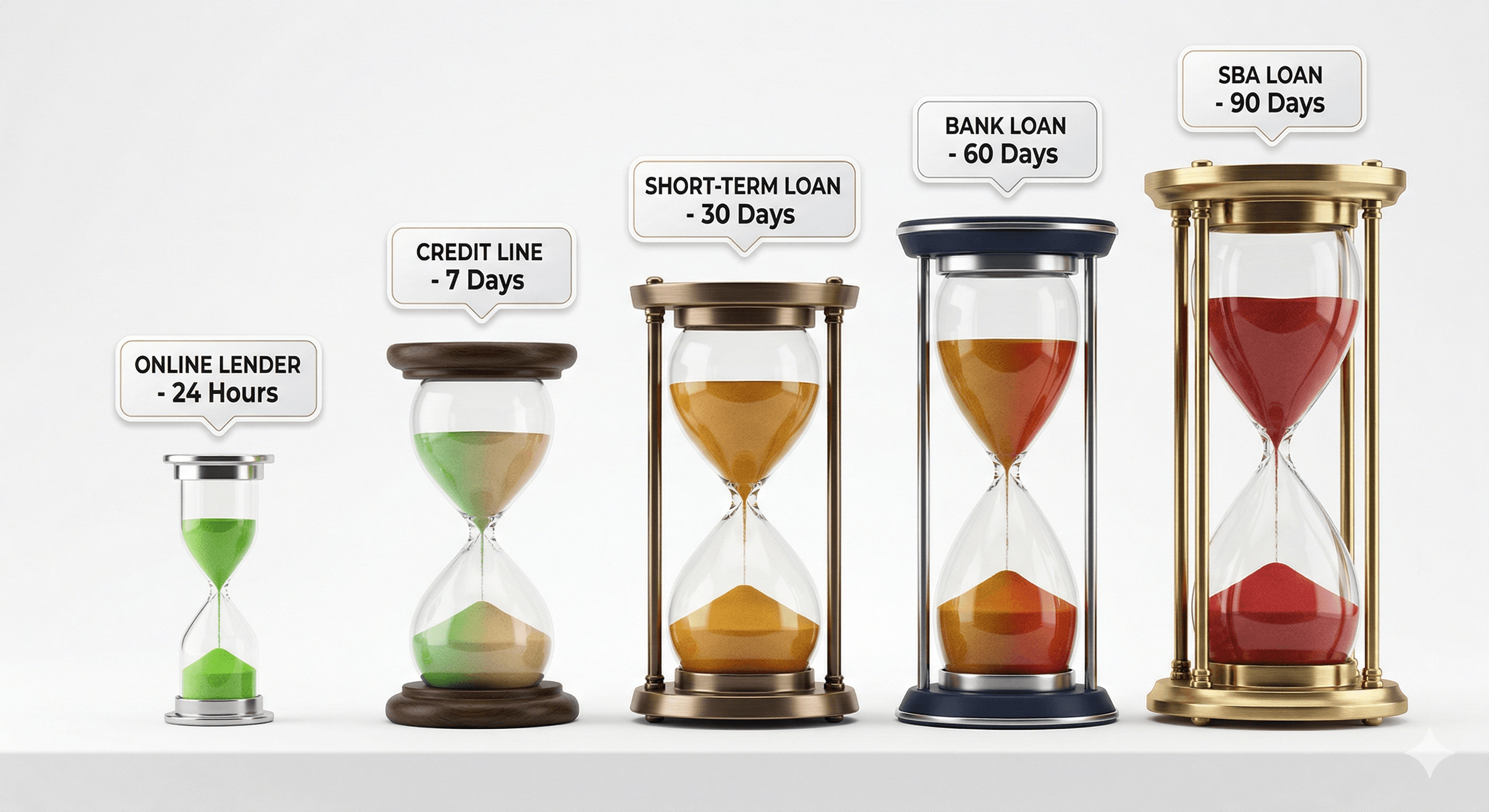

Small business loan approval times range from a few hours to 90 days, depending entirely on the lender type. Fintech and online lenders approve in hours to a few days. Credit unions take 1 to 2 weeks. Banks take 2 to 5 weeks. SBA loans take 2 to 4 weeks through a Preferred Lender, or 45 to 90 days through a standard SBA lender.

Quick answer: Fintech/AI lenders: 1 to 2 days. Online lenders: 1 to 3 days. Credit unions: 1 to 2 weeks. Community banks: 2 to 3 weeks. Big banks: 2 to 5 weeks. SBA Express and SBA 7(a) via PLP: 2 to 4 weeks. Standard SBA 7(a): 45 to 90 days. SBA 504: 60 to 90 days.

This guide breaks down approval timelines for every major lender type, what drives delays at each, and how to pick the right one for your timeline.

Approval times by lender type: master table

| Lender type | Application time | Approval decision | Funding | Total timeline |

|---|---|---|---|---|

| Merchant cash advance | 10 to 20 min | Same day | Same day to 24 hrs | 1 to 2 days |

| Online lender (automated) | 15 to 30 min | 2 to 24 hrs | 24 to 48 hrs | 1 to 3 days |

| Online lender (manual review) | 15 to 30 min | 1 to 3 days | 1 to 2 days | 2 to 5 days |

| Fintech / AI-powered lender | 10 to 20 min | 1 to 4 hrs | 24 to 48 hrs | 1 to 2 days |

| Credit union | 30 to 60 min | 3 to 7 days | 3 to 5 days | 1 to 2 weeks |

| Community bank | 1 to 2 hrs | 1 to 2 weeks | 3 to 5 days | 2 to 3 weeks |

| Traditional bank | 1 to 3 hrs | 1 to 3 weeks | 1 to 2 weeks | 2 to 5 weeks |

| SBA Express loan | 2 to 3 hrs | 36-hour SBA response | 1 to 2 weeks | 2 to 4 weeks |

| SBA 7(a) via PLP lender | 2 to 4 hrs | 1 to 2 weeks | 1 to 2 weeks | 2 to 4 weeks |

| SBA 7(a) standard lender | 2 to 5 hrs | 3 to 6 weeks | 1 to 2 weeks | 45 to 90 days |

| SBA 504 loan | 3 to 6 hrs | 4 to 8 weeks | 2 to 4 weeks | 60 to 90 days |

Lender type breakdown

Fintech and AI-powered lenders: 1 to 2 days

The fastest category. These lenders use machine learning to analyze bank statements and revenue in real time, issuing decisions in as little as 1 to 4 hours for straightforward applications. You connect your business bank account directly (open banking), the platform analyzes 3 to 12 months of transaction data instantly, and an algorithm generates an offer with no human underwriting. Best for established businesses with clean bank histories doing $50,000+ per month. Watch for higher rates: 20% to 50% APR is common. The speed premium is real.

Online lenders (automated underwriting): 1 to 3 days

The most popular category for small business lending. Lenders such as Bluevine, Fundbox, OnDeck, and Credibly use automated underwriting that processes applications faster than any bank. Application 15 to 30 minutes, decision 2 to 24 hours, funding 24 to 48 hours via ACH. Most work with scores from 580 to 600 and up. Loan amounts $5,000 to $500,000.

Online lenders (manual review): 2 to 5 days

When loan amounts are larger, credit is more complex, or automated systems flag an application, online lenders shift to manual underwriting. Triggers include requests above $150,000 to $250,000, scores below the automated threshold, inconsistent cash flow, very recent business history, or industry risk flags.

Credit unions: 1 to 2 weeks

Member-owned cooperatives that often offer lower rates than commercial banks (7% to 18% APR for qualified borrowers) with slower processing than online lenders. You must be a member to apply. Membership eligibility varies by institution.

Community banks: 2 to 3 weeks

The middle ground between national banks and online lenders. Relationship-based lending with more flexibility than national banks for seasonal businesses, recent credit events, or industries national banks decline. A strong existing relationship accelerates the process. Loan amounts $25,000 to $1,000,000+.

Traditional banks (large national banks): 2 to 5 weeks

The most competitive rates for highly qualified borrowers (6% to 15% APR) but the most rigorous process outside SBA lending. Typical minimums: 680+ personal credit, 2+ years in business, $100,000 to $250,000+ annual revenue, existing relationship preferred. Slower because of multiple layers of human review and credit committee approval. For a $500,000 loan, the rate gap versus an online lender can save $50,000 to $100,000 in total interest, worth the wait for the right borrower.

SBA Express loans: 2 to 4 weeks

The fastest SBA-backed product. The SBA commits to a 36-hour response on Express applications. Capped at $500,000 with a 50% guarantee (vs 75% to 85% on standard 7(a)), so lenders carry more risk and may apply stricter credit requirements.

SBA 7(a) via Preferred Lender (PLP): 2 to 4 weeks

PLP lenders can approve 7(a) loans in-house without submitting to the SBA for review. Standard SBA lenders must submit to the SBA, adding 2 to 4 weeks. For a loan that qualifies for both, a PLP lender saves 2 to 6 weeks with no other trade-off. Ask directly: "Are you an SBA Preferred Lender?" or check the SBA lender database.

SBA 7(a) standard lender: 45 to 90 days

The longest mainstream timeline, but access to the most favorable long-term rates (10.5% to 16.5% APR) and highest amounts (up to $5 million). Repayment terms up to 25 years for real estate. For planned long-term investments, no other product competes on total cost.

What causes approval delays, by lender type

| Lender type | #1 cause of delay | How to avoid it |

|---|---|---|

| Online lender | Incomplete application | Have all documents ready before starting |

| Fintech / AI lender | Bank connection issues | Use direct bank integration, not manual uploads |

| Credit union | Scheduling delays | Book the appointment before gathering documents |

| Community bank | Missing financial statements | Prepare P&L and balance sheet in advance |

| Traditional bank | Incomplete credit package | Pre-screen with a banker before applying |

| SBA Express | Slow borrower responses | Treat every lender request as same-day urgent |

| SBA PLP | Appraisal scheduling | Request the appraisal at application, not after approval |

| SBA standard | SBA review queue | Apply in Q2/Q3, avoid Q4 high-volume periods |

How to choose the right lender for your timeline

If you need funding in under 1 week: Online and fintech lenders are your realistic options. Accept higher rates and focus on the best offer in that category.

If you can wait 2 to 4 weeks: SBA Express or PLP lenders open up, giving government-backed rates without the 90-day wait. Credit unions too if you are a member and the amount fits.

If you can wait 1 to 3 months: Standard SBA 7(a) becomes viable, and for amounts over $500,000 or where total interest savings matter, the wait is often worth it.

If you are a startup or need under $50,000: SBA Microloans offer $500 to $50,000 with more accessible requirements than standard SBA programs.

If you are not sure which lender fits: A matching service like TopFunders.ai checks your profile against 30+ vetted lenders and connects you with the single best-fit option, including estimated rate and timeline, using a soft check that does not affect your credit score and requires no SSN or Tax ID to match.

Trends affecting approval times

- AI underwriting is getting faster. Models analyzing bank statement data in real time have compressed automated approvals from hours to minutes at leading fintech lenders.

- Open banking is removing document uploads. Direct bank connections verify 12 months of history in seconds, eliminating the statement-upload step that added 1 to 2 days.

- SBA processing has improved. Digital infrastructure investment has reduced standard review times. PLP lenders see faster internal processing from improved workflow tools.

- Weekend processing is expanding. Several online lenders offer 24/7 automated underwriting, so a Saturday-evening application can be approved by Monday morning.

- Appraiser bottlenecks persist. For secured loans needing real estate appraisals, appraiser availability remains constrained. Appraisal waits of 2 to 4 weeks are the single biggest delay in secured lending.

Frequently Asked Questions

How long does small business loan approval take?

It ranges from a few hours (fintech and online lenders) to 90 days (standard SBA 7(a)). The most common online lender timeline is 1 to 3 days. Banks take 2 to 5 weeks. SBA loans range from 2 to 4 weeks (Express and PLP) to 45 to 90 days (standard).

What is the fastest small business loan approval?

Fintech and AI-powered lenders are fastest, sometimes within 1 to 4 hours for straightforward applications. Merchant cash advances fund same-day. Automated online term loans and lines of credit typically fund within 24 to 48 hours of approval.

How long does a bank take to approve a small business loan?

Large banks typically take 2 to 5 weeks. Community banks are faster at 2 to 3 weeks. Credit unions take 1 to 2 weeks. The length is due to multiple layers of human review and credit committee approval.

How long does SBA loan approval take?

SBA Express: 2 to 4 weeks. SBA 7(a) via a Preferred Lender: 2 to 4 weeks. Standard SBA 7(a): 45 to 90 days. SBA 504: 60 to 90 days.

Why do some lenders approve loans faster than others?

It comes down to underwriting method. Fintech and online lenders use automated systems that analyze data in real time with no human review for straightforward applications. Banks and SBA lenders use human underwriters and multiple approval stages, more thorough but slower.

Does applying to multiple lenders at once speed up the process?

No. Multiple applications create multiple hard inquiries that can lower your score and may hurt your odds. A better approach is a matching service that identifies the single best-fit lender using a soft check, so you apply once to the right place.

What can I do to get approved faster regardless of lender?

Prepare a complete document package before applying: bank statements, tax returns, P&L, registration. Incomplete applications are the most common delay across all lender types. Respond to every lender request the same day.

Is a faster loan always better?

No. Faster loans (online, fintech) usually carry higher rates than slower options (banks, SBA). The right choice depends on your timeline, amount, and how much the rate difference costs over the term. On a $500,000 loan, 8% versus 25% is a large difference worth waiting for if your situation allows.

The bottom line

Understanding approval times by lender type lets you match your funding choice to your actual timeline rather than discovering three weeks in that you needed money last week. The fastest path is not always the right path. Weigh speed against cost and amount. The best first step: check your best-fit options across lender types before committing, so you see real timelines, rates, and amounts specific to your profile.

Find the lender that fits your timeline at TopFunders.ai. One match, no SSN or Tax ID required, no credit score impact.