In This Article

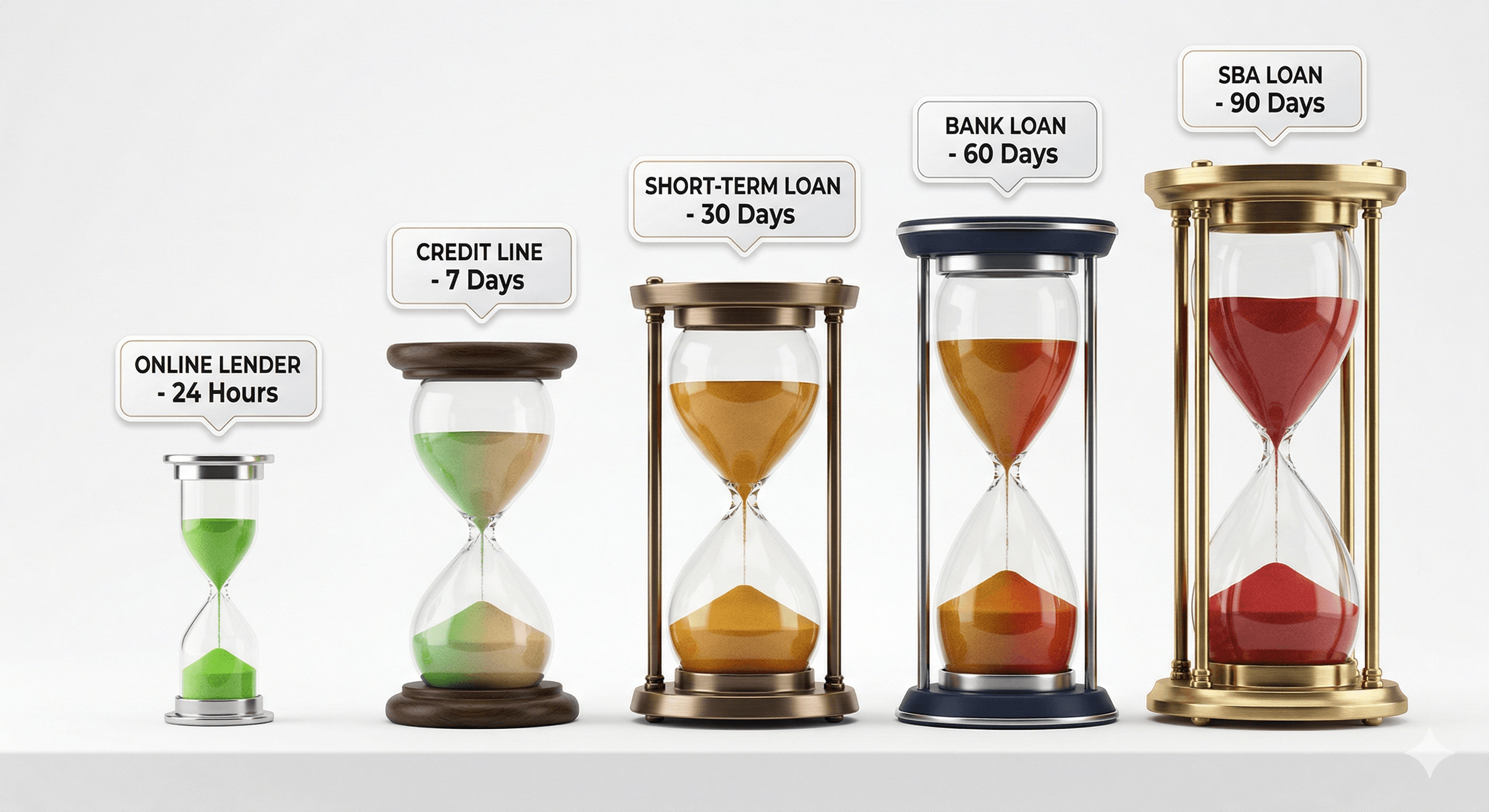

A business loan takes anywhere from 24 hours to 90 days, depending on the lender and loan type. Merchant cash advances and online term loans fund in 1 to 4 days. Bank term loans take 2 to 4 weeks. SBA loans take 30 to 90 days. The single biggest delay across every lender is an incomplete application.

Quick answer: Fastest is a merchant cash advance (same day, but most expensive). Online term loans and lines of credit fund in 1 to 5 days. Bank loans take 2 to 4 weeks. SBA 7(a) takes 30 to 90 days, or 2 to 4 weeks through a Preferred Lender. Match your timeline to the right loan type before you apply.

This guide breaks down how long each loan type takes, from application to funding, and how to speed it up.

Business loan timeline at a glance

| Loan type | Application time | Approval time | Funding time | Total timeline |

|---|---|---|---|---|

| Merchant cash advance | 10 to 20 min | Same day | Same day to 24 hrs | 1 to 2 days |

| Online term loan | 15 to 30 min | 24 to 48 hrs | 24 to 48 hrs | 1 to 4 days |

| Business line of credit (online) | 15 to 30 min | 24 to 72 hrs | 24 to 72 hrs | 2 to 5 days |

| Invoice financing | 20 to 40 min | 24 to 48 hrs | 24 to 72 hrs | 2 to 5 days |

| Equipment financing | 30 to 60 min | 2 to 5 days | 2 to 7 days | 3 to 10 days |

| Bank term loan | 1 to 3 hrs | 1 to 2 weeks | 1 to 2 weeks | 2 to 4 weeks |

| SBA 7(a) loan | 2 to 5 hrs | 2 to 4 weeks | 1 to 2 weeks | 30 to 90 days |

| SBA 504 loan | 3 to 6 hrs | 4 to 6 weeks | 2 to 4 weeks | 60 to 90 days |

How long each loan type takes

Merchant cash advance: 1 to 2 days

The fastest financing available. You receive a lump sum in exchange for a percentage of future daily sales. Application is minimal, often just a few months of bank statements.

The trade-off: MCAs are the most expensive form of business financing, with effective APRs that can reach 40% to 350%. Speed comes at a significant cost. Use only when capital is urgent and no other option exists.

Online term loan: 1 to 4 days

Online lenders use automated underwriting that issues decisions in hours rather than weeks. Application is 15 to 30 minutes, decision in 24 to 48 hours, funding 24 to 48 hours after approval.

What speeds it up: Having bank statements, tax returns, and business documents ready before you start. Incomplete applications are the most common delay with online lenders.

Business line of credit (online): 2 to 5 days

Initial approval takes 24 to 72 hours. Once approved, future draws are often available within hours, making it one of the most responsive tools for ongoing needs. You do not reapply each time you need funds.

Invoice financing: 2 to 5 days

You advance 80% to 95% of outstanding customer invoices. The lender weighs your customers' creditworthiness more than your own, which can speed approval. Best for B2B businesses with reliable customers but slow net-30, net-60, or net-90 payment cycles.

Equipment financing: 3 to 10 days

The equipment secures the loan, which gives lenders confidence and generally produces faster approvals than unsecured products at comparable amounts. The slight delay versus online loans comes from equipment verification. Have a vendor quote or purchase agreement ready when you apply.

Bank term loan: 2 to 4 weeks

Banks offer the most competitive rates for qualified borrowers, but underwriting is more complex and involves human review at multiple stages. A complete, error-free document package from day one is the biggest accelerator. An existing banking relationship also helps.

SBA 7(a) loan: 30 to 90 days

SBA loans offer some of the most favorable terms available: low rates, long terms, high amounts. The trade-off is a rigorous, document-heavy process. The SBA publishes program rules on its site. Working with a Preferred Lender Program (PLP) lender, who can approve without sending the loan to the SBA for review, cuts weeks off the process. SBA Express carries a 36-hour SBA response commitment.

SBA 504 loan: 60 to 90 days

For major fixed-asset purchases, commercial real estate, large equipment, facility improvements. It involves two lenders (a bank and a Certified Development Company), which adds time. The right choice for a major long-term investment when you have time to do it properly.

What affects your personal timeline?

- Documentation readiness. The biggest cause of delay across every lender type. Have bank statements, tax returns, P&L, and registration ready before applying.

- Credit profile complexity. Errors, disputes, or unusual items make underwriters spend more time verifying.

- Loan amount. Larger loans get more thorough review. A $30,000 online loan may fund in 24 hours; $300,000 from the same lender may take 5 to 7 days.

- Application accuracy. Errors trigger manual review.

- Lender volume. Applying mid-week (Tuesday to Thursday) often processes faster than Monday or Friday.

How to get a business loan faster: 6 steps

- Prepare documents before you start. 3 to 6 months of bank statements, 2 years of tax returns, a current P&L, and registration, in one folder ready to upload.

- Check your credit before applying. Pull personal and business reports, resolve errors, know your score going in.

- Use soft-check matching first. A matching service like TopFunders.ai shows the single best-fit lender for your profile using a soft check, with no SSN or Tax ID required and no credit score impact, so you avoid hard inquiries from lenders unlikely to approve you.

- Be specific about loan purpose. "Purchasing $45,000 of inventory for a confirmed contract" clears faster than "working capital".

- Respond to lender requests immediately. Every hour of delay is an hour added to your timeline.

- Match to one right lender instead of applying to many. Rather than several applications and several waiting periods, one targeted match to the best-fit lender removes the trial-and-error cycle.

Frequently Asked Questions

How long does it take to get a small business loan?

It depends on lender and loan type. Online lenders fund in 24 to 72 hours. Bank loans take 2 to 4 weeks. SBA loans take 30 to 90 days. The fastest option is a merchant cash advance (same day), which is also the most expensive.

What is the fastest type of business loan?

Merchant cash advances fund fastest, often same day or within 24 hours. Online term loans and lines of credit are next, typically 1 to 4 business days. If speed is the priority, online lenders almost always beat banks or SBA programs.

How long does SBA loan approval take?

Standard SBA 7(a) loans take 30 to 90 days. SBA Express has a 36-hour SBA response commitment, though total funding still runs about 2 to 3 weeks. A Preferred Lender (PLP) significantly reduces the timeline.

Can I get a business loan the same day?

Yes. Merchant cash advances and some online lenders offer same-day or next-day funding for qualifying businesses, usually for amounts under $100,000. Requirements are minimal but costs are high.

What slows down business loan approval?

Incomplete documentation, application errors, low credit requiring extra review, large loan amounts requiring deeper underwriting, and slow responses to lender requests. Having documents ready and responding same-day are the two highest-impact accelerators.

Does using a matching service speed things up?

Yes. Instead of applying to one lender, waiting, and restarting if rejected, a matching service identifies the single best-fit lender for your profile upfront so you apply once to the right place. This removes weeks of trial and error and avoids stacked hard inquiries.

How long does it take to get a business line of credit?

Online lines of credit typically take 2 to 5 days for initial approval and first draw. After the line is established, future draws are often available within hours, one of the most responsive ongoing funding tools available.

The bottom line

Knowing how long a business loan takes before you apply puts you in control. Match your timeline need to the right loan type and you avoid applying for a 90-day SBA loan when you need capital in two weeks. The fastest path is not always the cheapest, so weigh speed against cost and amount, and match to the right lender before committing.

Find the lender that fits your timeline at TopFunders.ai. One match, no SSN or Tax ID required, no credit score impact.