In This Article

Unsecured business loans are approved faster than secured ones, usually by weeks. An unsecured online loan can fund in 1 to 4 days because there is no collateral to appraise. A secured loan adds appraisal, title search, UCC filing, and legal documentation, pushing real-estate-secured loans to 6 to 12 weeks. The one exception is equipment financing, which closes in 3 to 10 days.

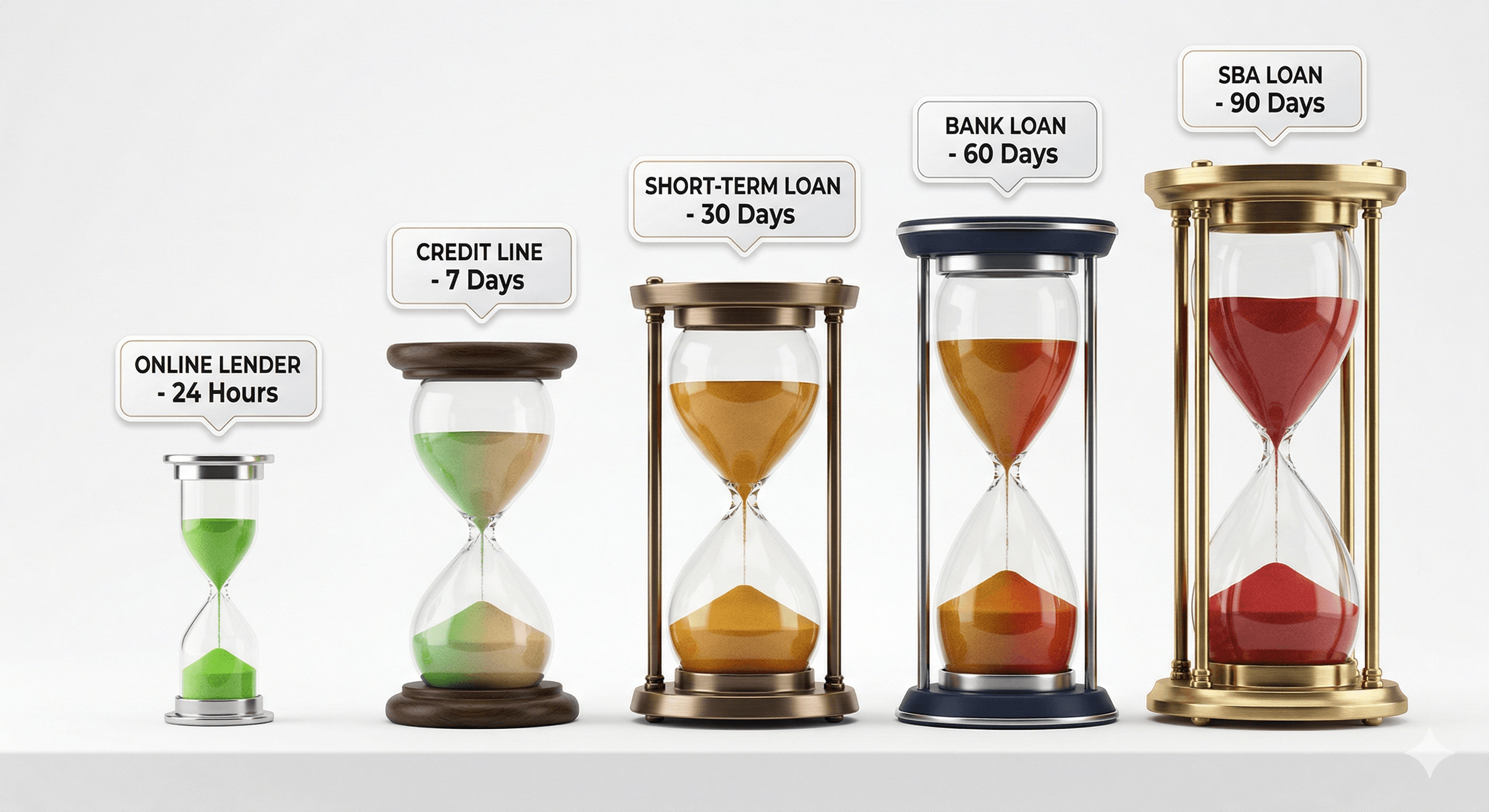

Quick answer: Unsecured wins on speed. Unsecured online loans: 1 to 4 days. Unsecured bank loans: 2 to 4 weeks. Secured equipment loans: 3 to 10 days. Secured bank loans: 3 to 6 weeks. SBA loans secured by real estate: 45 to 90 days. Collateral verification is what adds the time.

This guide breaks down the approval timeline for both loan types across every major lender.

Secured vs unsecured: the key difference

A secured business loan requires collateral, a physical asset such as real estate, equipment, or inventory the lender can claim if you default. Because the lender has a tangible safety net, rates are lower and amounts higher.

An unsecured business loan requires no collateral. Approval is based on your business's financial profile: credit score, revenue, cash flow, and time in business. The lender takes more risk, so rates are higher, but the process is faster.

That speed difference is the critical point. Collateral has to be identified, appraised, verified, and legally documented. Every one of those steps adds time.

Approval time comparison: secured vs unsecured

| Loan type | Collateral | Approval time | Funding time | Total timeline |

|---|---|---|---|---|

| Unsecured online term loan | None | 24 to 48 hrs | 24 to 48 hrs | 1 to 4 days |

| Unsecured line of credit (online) | None | 24 to 72 hrs | 24 to 72 hrs | 2 to 5 days |

| Unsecured bank term loan | None | 1 to 2 weeks | 1 to 2 weeks | 2 to 4 weeks |

| Secured equipment loan | Equipment | 2 to 5 days | 2 to 7 days | 3 to 10 days |

| Secured bank term loan | Real estate/assets | 2 to 4 weeks | 1 to 2 weeks | 3 to 6 weeks |

| SBA 7(a) unsecured (under $50K) | None | 2 to 4 weeks | 1 to 2 weeks | 30 to 45 days |

| SBA 7(a) secured (over $50K) | Assets required | 3 to 6 weeks | 1 to 2 weeks | 45 to 90 days |

| SBA 504 loan | Real estate/equipment | 4 to 8 weeks | 2 to 4 weeks | 60 to 90 days |

| Commercial real estate loan | Property | 4 to 8 weeks | 2 to 4 weeks | 60 to 90 days |

Why unsecured loans are approved faster

The speed advantage comes from one thing: no collateral verification process. A secured loan adds steps that simply do not exist with unsecured lending:

- Asset appraisal. Commercial property appraisal alone takes 1 to 3 weeks. Equipment is typically 2 to 5 business days.

- Title search. Verifying collateral is free of existing liens takes 1 to 2 weeks on real estate.

- UCC filing. Filing a Uniform Commercial Code statement to establish the security interest adds 1 to 3 business days.

- Insurance verification. Collateral must be insured and verified before closing.

- Legal documentation. Security agreements and, for real estate, deed of trust or mortgage documentation add days to weeks of legal review.

An online lender reviewing an unsecured application is looking at bank statements and a credit score, a process that takes hours, not weeks.

Unsecured approval timeline, step by step

The fastest path, an unsecured online loan:

- Hour 0 to 1: 15 to 30 minute online application, bank statements uploaded digitally.

- Hour 1 to 24: Automated underwriting analyzes statements, verifies revenue, checks credit. Fully automated for straightforward applications.

- Hour 24 to 48: Decision and offer with a specific amount, rate, and term. Strong profiles sometimes get decisions in 4 to 8 hours.

- Hour 48 to 72: Funding after you accept and e-sign. Same-day ACH with some lenders; standard ACH 1 to 2 business days.

Total: 1 to 4 days.

Secured approval timeline, step by step

A secured bank term loan collateralized by commercial real estate, the most thorough process:

- Days 1 to 3: Application plus extensive documentation and preliminary collateral information.

- Days 3 to 10: Initial underwriting review, with document requests common.

- Days 7 to 21: Independent collateral appraisal.

- Days 14 to 28: Title search and legal documentation review.

- Days 25 to 42: Credit committee approval and commitment letter.

- Days 35 to 55: Closing, executing legal documents, recording liens, verifying insurance, UCC filings.

- Days 42 to 60+: Funding after closing conditions are satisfied.

Total: 6 to 12 weeks minimum for real-estate-secured loans.

Which is faster: secured or unsecured?

In almost every scenario, unsecured business loans are faster, often dramatically so. The one exception is equipment financing: because the equipment serves as collateral and can be verified quickly via invoice or purchase agreement, equipment loans from specialized lenders close in 3 to 10 days, competitive with some unsecured online loans. Outside equipment financing, collateral verification adds weeks that cannot be compressed.

When waiting for a secured loan is worth it

- You need a large amount. Unsecured loans top out around $250,000 to $500,000 with most lenders. For $750,000+, secured lending or SBA programs is likely the only path.

- You want the lowest rate. On a $500,000 loan, the secured-vs-unsecured rate difference can save $30,000 to $80,000 in total interest.

- You have a long runway. A planned property purchase or major expansion gives you time to do it properly.

- You are applying for an SBA loan. SBA 7(a) loans over $50,000 typically require collateral when available, with government-backed rates that are hard to match.

How to speed up either loan type

- Have documents ready before applying. 3 to 6 months of bank statements, 2 years of tax returns, a current P&L.

- Apply mid-week. Tuesday through Thursday tends to process faster than Monday or Friday.

- Respond to lender requests the same day. Every hour of delay adds to the timeline.

- Match to the right lender first. Applying to a lender whose criteria do not fit means rejection and wasted time. A matching service like TopFunders.ai checks your profile against 30+ vetted lenders and connects you with the single best-fit option, with no SSN or Tax ID to match and no credit score impact.

- For secured loans, order the appraisal early. Appraisal is often the longest single step; starting it early compresses the total timeline.

Trends affecting approval times

- AI underwriting is compressing unsecured timelines. Real-time bank statement analysis reduces decisions from days to hours for straightforward applications.

- SBA processing has improved. Digital infrastructure has cut average 7(a) review times. PLP lenders approve without waiting for SBA review.

- Commercial appraisals remain slow. Appraiser capacity has not kept pace with demand; 3 to 4 week waits are common in competitive markets.

- Open banking accelerates verification. Direct bank connections verify income and cash flow in minutes rather than days.

Frequently Asked Questions

How long does it take to get an unsecured business loan?

Online lenders can approve and fund unsecured business loans in 24 to 72 hours. Unsecured bank loans take 2 to 4 weeks. The fastest option, from specialized online lenders, can fund the same day for strong profiles.

How long does it take to get a secured business loan?

Equipment loans close in 3 to 10 days. Secured bank term loans take 3 to 6 weeks. SBA loans secured by real estate take 45 to 90 days.

Why does collateral slow down loan approval?

Collateral adds mandatory steps that cannot be skipped: appraisal, title search, UCC filing, insurance verification, and expanded legal documentation. Each depends on third parties (appraisers, title companies, attorneys) on their own schedules.

Can a secured business loan be faster than an unsecured one?

In rare cases, yes, specifically equipment financing. Equipment is easy to verify via purchase invoice and has a clear market value, so equipment loans can close in 3 to 7 days. For all other secured types, unsecured is faster.

What is the fastest type of business loan available?

Merchant cash advances fund fastest, sometimes same day. Among traditional products, unsecured online term loans and lines of credit are fastest, typically 24 to 72 hours. AI-powered lenders sometimes decide in under 4 hours.

Does applying for a secured or unsecured loan affect my credit score?

Both involve a hard inquiry when you formally apply, which can temporarily lower your score by 2 to 5 points. A soft-check matching service like TopFunders.ai lets you identify the right loan type and lender before any hard inquiry, with no SSN or Tax ID required.

Is it harder to qualify for a secured or unsecured business loan?

It depends on what you have. If you own significant assets, a secured loan can be easier to qualify for, the collateral reduces the lender's risk and offsets weaker credit or revenue. Unsecured loans rely entirely on your financial profile.

The bottom line

The speed gap between secured and unsecured business loans is wide. AI underwriting has made unsecured online loans faster, while appraisal backlogs have made some secured loans slower. If speed is the priority, unsecured online lending wins by a significant margin. If loan size, rate, or access to government-backed programs matters more, a secured loan may be worth the longer wait. Before applying to either, check your best-fit options for both types in minutes, at no cost and with no credit score impact.

Find the loan type and lender that fit your profile at TopFunders.ai. One match, no SSN or Tax ID required, no credit score impact.