In This Article

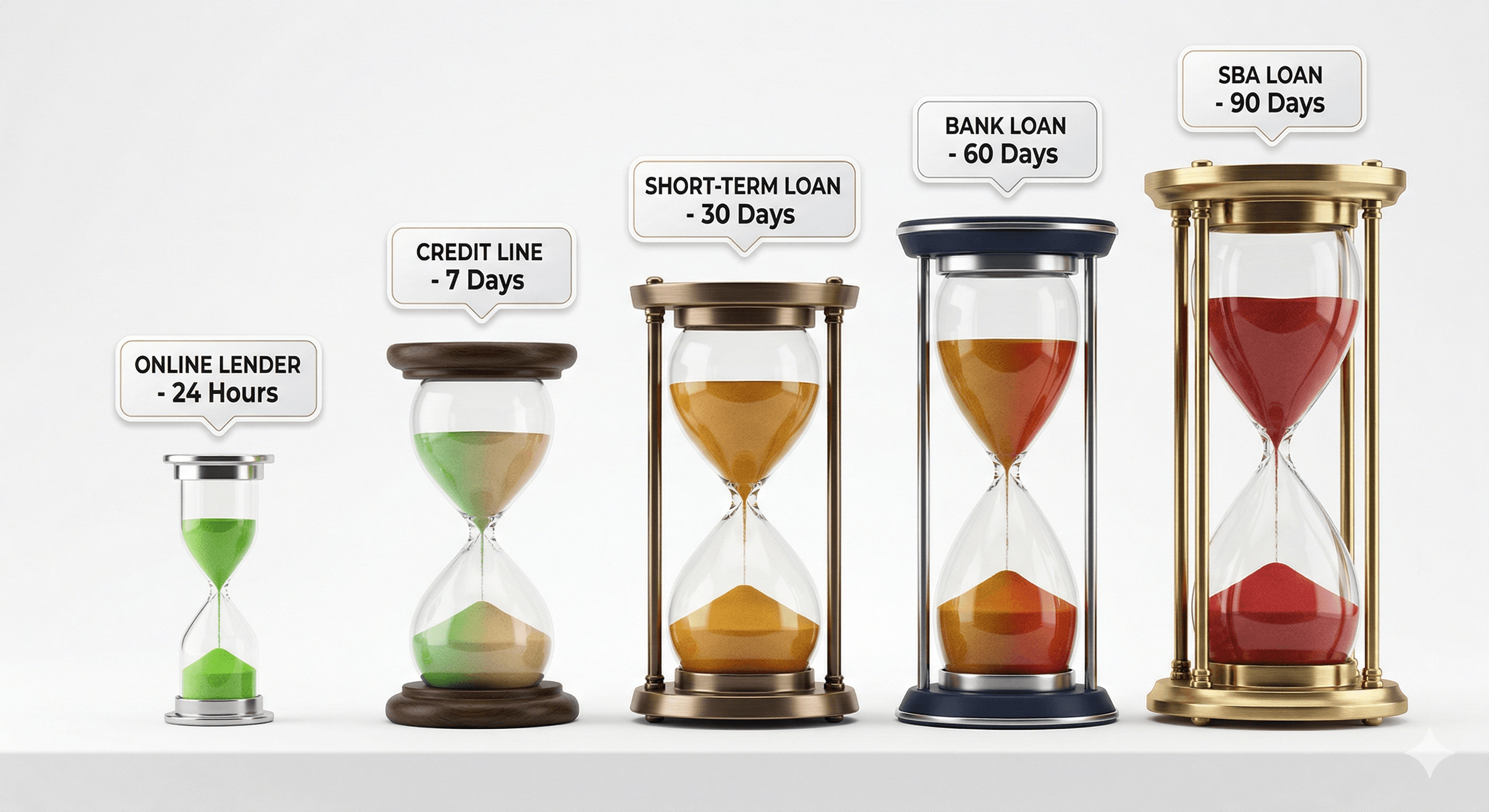

An SBA 7(a) loan takes 30 to 90 days from application to funding. Through an SBA Preferred Lender (PLP) the timeline drops to 2 to 4 weeks, because a PLP approves the loan in-house without sending it to the SBA for review. The SBA Express option gives a 36-hour SBA response and funds in 2 to 4 weeks.

Quick answer: Standard SBA 7(a): 45 to 90 days. SBA 7(a) through a Preferred Lender: 2 to 4 weeks. SBA Express: 2 to 4 weeks with a 36-hour SBA response. The three biggest timeline factors are lender type, application completeness, and how fast you respond during underwriting.

This guide breaks down every stage of the SBA 7(a) process, what causes delays, and the fastest legitimate path to funding.

SBA 7(a) processing time at a glance

| Lender type | Approval time | Funding time | Total timeline |

|---|---|---|---|

| SBA Preferred Lender (PLP) | 1 to 2 weeks | 1 to 2 weeks | 2 to 4 weeks |

| SBA Certified Lender (CLP) | 2 to 3 weeks | 1 to 2 weeks | 3 to 5 weeks |

| Standard SBA lender | 4 to 8 weeks | 1 to 2 weeks | 45 to 90 days |

| SBA Express | 36-hour SBA response | 1 to 3 weeks | 2 to 4 weeks |

| SBA Small Loan ($50K and under) | 1 to 2 weeks | 1 week | 2 to 3 weeks |

What is an SBA 7(a) loan?

The SBA 7(a) loan is the US Small Business Administration's primary lending program. The SBA does not lend money directly. It guarantees part of a loan made by an approved lender, which lowers the lender's risk and lets them offer better terms. Full program rules are published on SBA.gov.

Key facts:

- Maximum loan amount: $5 million

- SBA guarantee: 85% on loans up to $150,000, 75% on loans above $150,000

- Interest rates: Prime rate plus 2.25% to 4.75% depending on size and term

- Repayment terms: Up to 10 years for working capital, up to 25 years for real estate

- Collateral: Required for loans over $50,000 when available

- Personal guarantee: Required from every owner with a 20% or larger stake

The full SBA 7(a) timeline, stage by stage

Stage 1: Pre-application and lender selection (1 to 5 days)

Before a formal application, you identify an SBA-approved lender and confirm basic eligibility. First-time applicants often skip this and add weeks to the process.

What speeds it up: Identifying the right SBA lender for your profile before you make contact. Not every SBA lender works with every business type or loan size. A matching service like TopFunders.ai checks your profile against 30+ vetted lenders and connects you with the single best-fit SBA lender, with no SSN or Tax ID required to match and no credit score impact.

Stage 2: Application and document submission (3 to 10 days)

The SBA 7(a) application needs far more documentation than an online loan. Incomplete applications get returned and reprocessed at the back of the queue. Typical documents:

- SBA Form 1919 (Borrower Information)

- SBA Form 912 (Statement of Personal History) if applicable

- Personal financial statement (SBA Form 413)

- 3 years of business tax returns

- 3 years of personal tax returns for owners with a 20%+ stake

- Year-to-date profit and loss statement and balance sheet

- Business debt schedule

- Use-of-proceeds statement

- Business licenses and legal documents

What speeds it up: A complete package on first submission moves straight to underwriting. An incomplete one bounces back and adds 1 to 3 weeks.

Stage 3: Lender underwriting (5 to 21 days)

This is where most timeline variation happens, and it depends on lender type.

- PLP lenders approve in-house without SBA review. Underwriting is usually 5 to 10 business days.

- CLP lenders get a 3-day SBA turnaround commitment. Underwriting is usually 10 to 15 business days.

- Standard SBA lenders send the full package to the SBA. That adds 5 to 10 business days on top of the lender's own work, extending underwriting to 3 to 6 weeks.

What speeds it up: Applying through a PLP lender. This single choice can remove 3 to 6 weeks versus a standard SBA lender.

Stage 4: SBA review and guarantee

For PLP lenders this stage effectively does not exist. For standard lenders, the SBA reviews the package and issues its guarantee. Review times rise during high-demand periods, typically Q4 and early Q1 around the federal fiscal year end.

Stage 5: Commitment letter and conditions (3 to 7 days)

The lender issues a commitment letter with the amount, rate, term, and conditions to satisfy before closing: updated financials, proof of insurance, collateral documentation, lien searches, and environmental assessments for real estate. Respond to every condition the same day to avoid pushing back the closing date.

Stage 6: Closing (5 to 14 days)

SBA closings involve more legal documents than conventional loans. Real estate loans add title insurance and recording. A lender with an experienced SBA closing team moves faster than one that handles SBA loans occasionally.

Stage 7: Funding (1 to 5 days after closing)

Funds are disbursed to your business bank account, usually in a single disbursement. Construction or renovation loans may fund in draws.

Total: 30 to 90 days from application to funding.

SBA Express: the fastest SBA option

If you want SBA-backed financing with the shortest timeline, the SBA Express loan is the fastest path in the 7(a) program.

| Feature | Standard SBA 7(a) | SBA Express |

|---|---|---|

| Maximum loan amount | $5,000,000 | $500,000 |

| SBA response time | 5 to 10 business days | 36 hours |

| SBA guarantee | 75% to 85% | 50% |

| Total timeline | 45 to 90 days | 2 to 4 weeks |

| Collateral requirement | Required over $50K | Lender discretion |

The SBA commits to a 36-hour response on SBA Express submissions. The trade-off is a lower 50% guarantee, so lenders carry more risk and may apply stricter credit requirements.

What causes SBA 7(a) delays?

- Incomplete application at submission. The most common cause by far. Missing documents send you to the back of the queue.

- Wrong lender type. A standard SBA lender adds 3 to 6 weeks versus a PLP for the same loan.

- Collateral appraisal delays. Real estate loans need appraisals, and appraiser availability is constrained in many markets (2 to 4 weeks is common).

- Slow responses during underwriting. Every day you delay a document request extends the process.

- Credit or financial surprises. Report errors, inconsistent documents, or unexplained cash flow trigger extra scrutiny.

- High-volume periods. Q4 and early Q1 process slower due to fiscal year-end demand.

SBA 7(a) vs alternative lenders: timeline and cost

| Option | Timeline | Rate range | Max amount |

|---|---|---|---|

| SBA Express | 2 to 4 weeks | 10.5% to 13% | $500,000 |

| SBA 7(a) via PLP lender | 2 to 4 weeks | 10.5% to 16.5% | $5,000,000 |

| SBA 7(a) standard | 45 to 90 days | 10.5% to 16.5% | $5,000,000 |

| Online term loan | 1 to 4 days | 15% to 45% | $500,000 |

| Bank term loan | 2 to 4 weeks | 6% to 20% | $1,000,000+ |

| Unsecured online lender | 24 to 72 hours | 20% to 60% | $250,000 |

The SBA 7(a) program consistently offers the best rates available to small businesses, but only for those who can wait. If you need capital in days, online lenders are faster at a higher cost.

Who qualifies for an SBA 7(a) loan?

Business eligibility: for-profit, US-based, meets SBA size standards for your industry, not in a prohibited industry, and unable to get reasonable conventional financing elsewhere.

Borrower eligibility: personal credit score of 620+ (most PLP lenders prefer 650 to 680+), US citizen or lawful permanent resident, no recent bankruptcies or outstanding tax liens, demonstrated repayment ability from business cash flow.

Time in business: The 7(a) program has no strict minimum, but most lenders want 2+ years. Earlier-stage businesses can use the SBA Microloan program instead.

How to get an SBA 7(a) loan faster: 6 steps

- Choose a PLP lender. The single highest-impact decision. Ask directly: "Are you an SBA Preferred Lender?"

- Prepare a complete document package before applying. A complete first submission enters underwriting immediately.

- Write a specific use-of-proceeds statement. Vague purposes slow review.

- Clean up your credit first. Dispute report errors and pay down revolving balances.

- Respond to every lender request same day. Treat each as your top priority.

- Use a matching service to find the right SBA lender. Rather than guessing, TopFunders.ai identifies the single PLP lender most likely to approve your specific profile, with no SSN or Tax ID to match and no credit score impact.

Frequently Asked Questions

How long does an SBA 7(a) loan take?

SBA 7(a) processing ranges from 2 to 4 weeks through a Preferred Lender (PLP) to 45 to 90 days through a standard SBA lender. SBA Express is the fastest SBA-backed option, with a 36-hour SBA response and total funding in 2 to 4 weeks.

What is the fastest way to get an SBA loan?

The fastest SBA option is the SBA Express program through a PLP lender. The combination of a 36-hour SBA response and in-house approval authority funds well-prepared applications in 2 to 4 weeks.

Why do SBA loans take so long?

SBA loans involve three parties, the borrower, the lender, and the SBA, each with its own review. Collateral appraisal, title searches, UCC filings, and complex legal documentation add time. Choosing a PLP lender removes the SBA review stage and compresses the timeline significantly.

Can I get an SBA loan in 30 days?

Yes. Through a PLP lender, with a complete application and same-day responses during underwriting, SBA 7(a) and SBA Express loans can fund in 30 days or less.

What credit score do I need for an SBA 7(a) loan?

The SBA publishes no minimum, but most SBA-approved lenders want a personal score of 620 to 650 minimum, and PLP lenders typically prefer 650 to 680+. A score of 700+ opens the widest range of lenders.

What is the maximum SBA 7(a) loan amount?

$5 million. The SBA Express subset is capped at $500,000. For real estate and major equipment, the SBA 504 program goes up to $5.5 million.

Do I need collateral for an SBA 7(a) loan?

The SBA requires lenders to take available collateral on loans over $50,000, but a lack of collateral does not automatically disqualify you. The SBA's guarantee reduces the collateral requirement compared to conventional lending.

How does an SBA 7(a) loan compare to online lenders?

SBA 7(a) loans carry far lower rates (10.5% to 16.5% vs 15% to 60% online) and much longer terms (up to 25 years vs 1 to 5). The trade-off is speed: online lenders fund in days, SBA loans in weeks to months. For businesses that can wait, SBA 7(a) almost always produces a lower total cost.

The bottom line

The SBA 7(a) program is one of the most powerful financing tools for US small businesses, but it rewards preparation and patience. The businesses that move fastest choose a PLP lender, submit complete applications, and respond immediately at every stage. If you need capital faster, an online lender can bridge the gap, and a matching service can show you both paths against your real profile rather than guesswork.

Find the SBA lender that fits your profile at TopFunders.ai. One match, no SSN or Tax ID required, no credit score impact.